Key Highlights

- We expect Red Sea crises and current weather conditions in the North of Europe and Panama to have a short term and mild impact only on affected individual ports.

- Primary ports of call are expected to have a milder impact and quicker recovery given more stable cash flows

- Delays on vessels given the longer alternative route through Cape of Good Hope will bring further temporary operational inefficiencies to affected ports while the situation is solved.

- Despite challenges, we expect the credit profiles of rated issuers to remain supported by fundamental factors.

Overview

We expect winter weather conditions in the North of Europe and current Red Sea instability to have a temporary negative effect on operations of container ports across Europe. We expect the Red Sea crisis to have bigger impact on East and South Mediterranean ports with some temporary reduction of volumes, whereas primary ports of call in the North of Europe are expected to experience limited impact and may even see phase pressure in yard capacity given delays due to longer trips. As a

mitigant to potential volume declines, ports in general have a proportion of their revenue under long term contracts and have some take-or-pay contracts that protect from further revenues volatility.

We expect primary ports of call, which are end destinations such as the Port of Rotterdam or Port of Antwerp, to have more protected volumes and therefore more stable cashflows. These ports have deep sea vessels access, good ingress and egress for vessels, are well connected by other types of transportation infrastructure with other countries in Europe, and offer a good variety of services, supporting stickiness of customers and protecting volumes.

On the other hand, other secondary ports of call, like the ones on East and South Mediterranean ports, which are a stopover on the way to the primary ports of call and are geographically more affected by the re-routing, are expected to face some temporary reductions on volumes. In these situations, we put a higher focus on long-term contracts, share of revenues, and liquidity on these ports and assess event driven scenarios with lower volumes. Ports with little buffer on liquidity and material and more prolonged drop of volumes with lower protections could have rating implications if the situation is not resolved soon. Still, so far data suggest a mild impact, but we will continue to monitor how the situation evolves. Overall, we expect these pressures to be resolved in the short run, with a more noticeable impact from mid-February once re-routed vessels start arriving to their final destinations.

The attacks on container vessels raise concerns about the safety of shipping lanes and the potential impact on global trade. In our commentary Credit Impact of Red Sea Shipping Disruption Varies by Industry, we discuss how sea cargo has been affected by an increase in sea vessel shipping rates. Also, in our commentary on Red Sea Crisis: War Insurance Rates to Increase Following U.S. and UK Airstrikes on Houthi Targets, we mention the impact of the attacks to commercial ships on war insurance rates to shipping companies, which is expected to increase, meaning further increases in shipping rates and that further attacks on commercial ships are expected. However, the United States, together with a multinational maritime coalition including the UK, Bahrain, Canada, and the Netherlands, have launched Operation Prosperity Guardian in the Red Sea and the Gulf of Aden, leading to expectations for a short-term solution providing some stability to the area.

As per our Global Container Terminal Operators 2024 Outlook, our ratings on container terminal

operators remain supported by fundamental factors such as the strength of the service areas served

by the terminal, competitive positioning of terminals, long-term concession agreements, and

demand for essential goods. With medium-term forecasts based on normalized growth and

companies having adequate liquidity, the credit profiles of rated Issuers are expected to remain

stable. For more information, see our Global Container Terminal Operators 2024 Outlook.

Red Sea Current Situation – Alternative Route Has Operational Implications in Affected Ports

Since November 2023, attacks on commercial ships in the Red Sea because of the Israel-Hamas

conflict, as well as recent Houthi attacks in the region, have been causing ships to avoid the Suez

Canal and use alternative routes through the south of Africa. The Suez Canal route is the main

maritime artery in the world, connecting Asia and Europe and representing about 15% of the

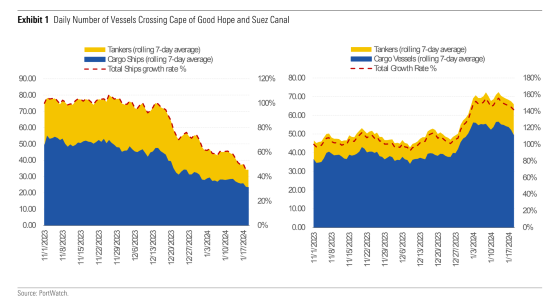

world´s shipping traffic. In January, container traffic dropped around 50% in the Suez Canal. We

expect this number to increase further in the next couple of weeks, with an anticipated 60%

reduction in shipping volumes or more if the situation is not resolved soon.

The alternative shipping route to avoid the Red Sea is though Cape of Good Hope, in South Africa,

creating significant congestion in bunkering ports around Africa and placing pressure on ports

infrastructure. This route is much longer, adds about 10 to 15 days on average, and results in ships

to heading directly to Northern Europe and West Mediterranean ports at the expense of East and

South Mediterranean ports. This means that the impact of the re-routing will start to be more

noticeable in port volumes beginning in mid-February. In January, volumes in affected ports have

seen little impact; however, we can already see the differences in flows on the crossings. These

numbers take into account the daily number of vessels, but not the size of the vessels.

Source: PortWatch.

Source: BBC

Primary Ports of Call More Protected from Operational Implications

Generally speaking, primary ports of call that are in the north of Europe and are the end destination

for vessels coming from the Middle East or Asia are expected to see their volumes to be more

protected from the conflicts. This is because the alternative route is still ending in those ports and

cash flows are expected to be more stable. Still, we do expect some temporary operational

inefficiencies that will create congestion in those ports given delays of ships that are using the

alternative route and are expected to arrive to the North of Europe around mid-February. This

situation has been exacerbated by bad weather conditions in that area and closure of terminals due to past holiday season.

We see more negative, albeit temporary, implications for the stopover ports on the commercial

route from the Middle East or Asia to Europe. Ports that would usually be used for stopovers on the

normal route will lose some of their volumes with bigger shipping companies that decide to either

reduce stops or go through the alternative route. However, data to date still reflect normal

operations and we expect to see some of the impact in February to show some of the impact,

though we expect this to be manageable, unless the instability in the Red Sea area is prolonged.

The longer route through Cape of Good Hope will add some extra days to the transit of the vessels,

creating port congestion over the coming weeks and operational inefficiencies due to limited yard

capacity. To this extent, we consider that some ports will be better prepared to absorb the increase

in volumes than other smaller and less prepared ports that would not normally be part of such a big commercial route.

In Africa, we expect some smaller and less prepared ports to exceed capacity with an impact on

operations. On the other hand, the Port of Tanger-Med is better prepared and has already seen an

increase in capacity with the recent expansion that became fully operational on 1 January this year.

With cheaper rates given government support, we would expect it to benefit from increased volumes.

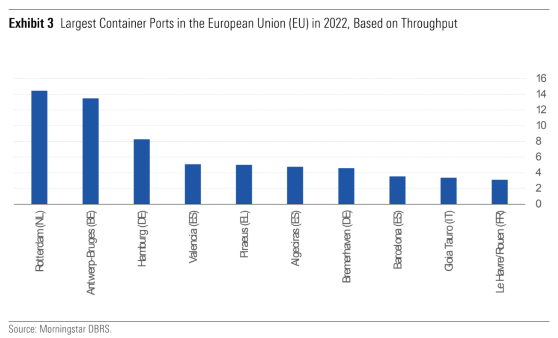

In the West Mediterranean ports in Europe, Port of Algeciras, the biggest port in Spain by gross

tonnage, and the Port of Valencia, the biggest container port in the country and the fourth-biggest

port in Europe, have sufficient capacity to withstand the situation and are expected to absorb a

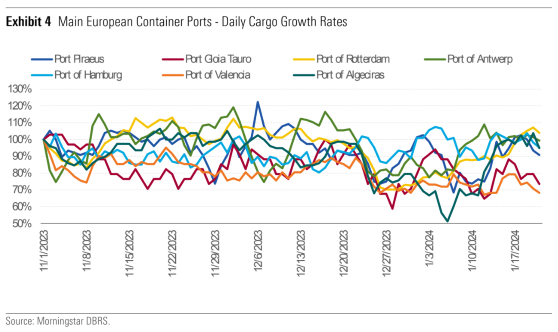

temporary increase in volumes. Main container ports in Spain initially saw a decrease in the number

of cargo ships in November following the Hamas attack on Israel on October 7, 2023. However,

most of these ports have fully recovered volumes, except Port of Valencia, which is still at around

80% compared to 1 November volumes. Again, these numbers don´t take into account the size of the vessels.

We expect Red Sea unrest to have a modest impact on ports in Northern Europe, including the Port

of Rotterdam, which is the biggest container port in Europe, and the Port of Antwerp, second

largest in Europe; both are considered primary ports of call in Europe. Port of Rotterdam Authority

foresees a decrease of approximately 1.25 million tonnes in December 2023 due to these

disruptions, which is very little compared with the total 467 million tonnes reported for 2022. Also,

the Port of Antwerp’s CEO expects to not lose any traffic because of the crisis and also expects

additional cargo to end up in Antwerp and Zeebrogge (Belgium) that would otherwise not end up in

those ports, possibly leading to congestion. Given the minimal impact and higher stability of cash

flows, we do not expect any potential credit implications from this issue in primary ports of call.

Since 1 November 2023, data shows that the Port of Rotterdam and the Port of Antwerp had

between a 20% to 30% drop each in the number of cargo ships in December, but it was a short-term

impact and is now fully recovered. Hamburg port operator HHLA and Eurogate (Germany) so far

have not been disrupted either but are prepared for shipping delays.

On the other hand, we expect ports in the East and Central Mediterranean to see a temporary drop

in their volumes until supply chains go back to normal. We expect these ports to potentially be the

most affected from the re-routing to Europe, with some possible congestion from February as we

expect the number of big vessels to decline. We foresee this area of the Mediterranean region to be

served by more trans-shipments from western hubs. With about 40% of Italy´s international

maritime trade relying on the Red Sea route, we see risks in particular related to Italian port

volumes. So far, number of cargo ships in the Genova Port (Italy) have decreased about 40% in

recent weeks having recovered now to a 20% reduction from 1 November volumes. Port of Gioia

(Italy) is also still around 80% from 1 November volumes in cargo.

In Greece, for the Port of Piraeus, the fifth-largest container port in Europe, volumes have so far

been quite stable with little impact from the disruptions. However, we expect drops of cargo around

30% or more in this port. We will continue to monitor the situation, especially once ships coming

from Asia and Middle East start arriving in Europe. Container shipping giants CMA CGM, Cosco

Container Lines, Evergreen Line, and Orient Overseas Container Line have decided to stop their tri

weekly routes from Asia to Piraeus, which was a stopover to northern Europe. At the same time,

Maersk and other container shipping companies have rerouted to Cape of Good Hope, which does

not enter into the East and Central Mediterranean Sea. Entering into the center of the

Mediterranean Sea adds extra days to the already longer route.

Extreme Weather Conditions Also Affect North Europe Ports and Panama Canal

Northern Europe has also faced other operational temporary issues. The Christmas holiday period

and unfavorable weather conditions have led to terminal closures and navigation stoppages.

Combined with the current situation in the Red Sea, yard density across terminals in that area is increasing.

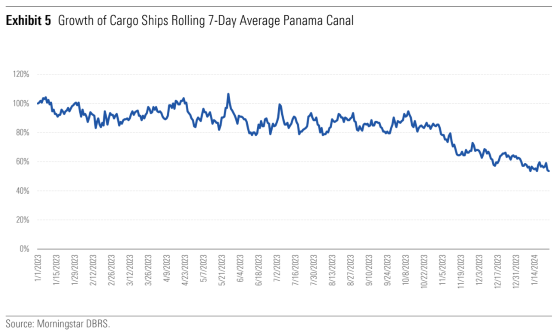

Low water levels in the Panama Canal due to severe droughts are also adding extra disruptions to global trade. Low water levels in the canal have severely reduced the number and size of vessels that can transit through it. The total number of transits through the Panama Canal is about 40% lower than a year ago. This is expected to also have an impact on ports in the U.S., with the East Coast potentially being more affected than the West Coast. Number of vessels coming from Asia to the U.S. are expected to have long delays; as well, the East Coast might experience a reduction on volumes. Some big shipping companies, like Maersk, have already announced their decision to use trains on the Panama Canal Railway to avoid the waterway. This could add to some further delays on southbound vessels. Again, it is still a bit too early to see the impact on data, but as weeks pass, we expect the impact to gradually ramp up.

Author, Ana Relanzon

Vice President, Credit Ratings

European Corporate Finance

Source, Morningstar DBRS

")